Form 1099-DA and the Limits of Broker-Based Reconciliation

Form 1099-DA is a meaningful development in digital asset tax administration. It is not a reconciliation foundation. What follows covers what the form structurally cannot do, what preparers and taxpayers should do instead, and why the data risks of uploading 1099-DA files to consumer platforms deserve careful attention.

Form 1099-DA, titled by the IRS "Digital Asset Proceeds From Broker Transactions," entered the reporting landscape for tax year 2025. Its arrival is a legitimate step toward transparency in digital asset taxation, and it will become a useful cross-reference for preparers and a meaningful audit tool for the IRS. What it is not, and what its design never intended it to be, is a foundation for reconciliation. The distinction matters because a growing number of taxpayers, preparers, and compliance teams are treating it as though the two functions are the same. They are not, and the consequences of conflating them range from inefficient workflows to materially incorrect returns.

This analysis makes three arguments. First, 1099-DA is structurally incapable of supporting authoritative reconciliation because of limitations built into the form itself. Second, there is a practical, defensible alternative that treats 1099-DA as a check rather than a source. Third, uploading or storing 1099-DA files in consumer-grade platforms introduces personal data risks that many filers have not fully considered.

Part I: Why 1099-DA Cannot Anchor Reconciliation

The Form Reports What the Broker Saw, Nothing More

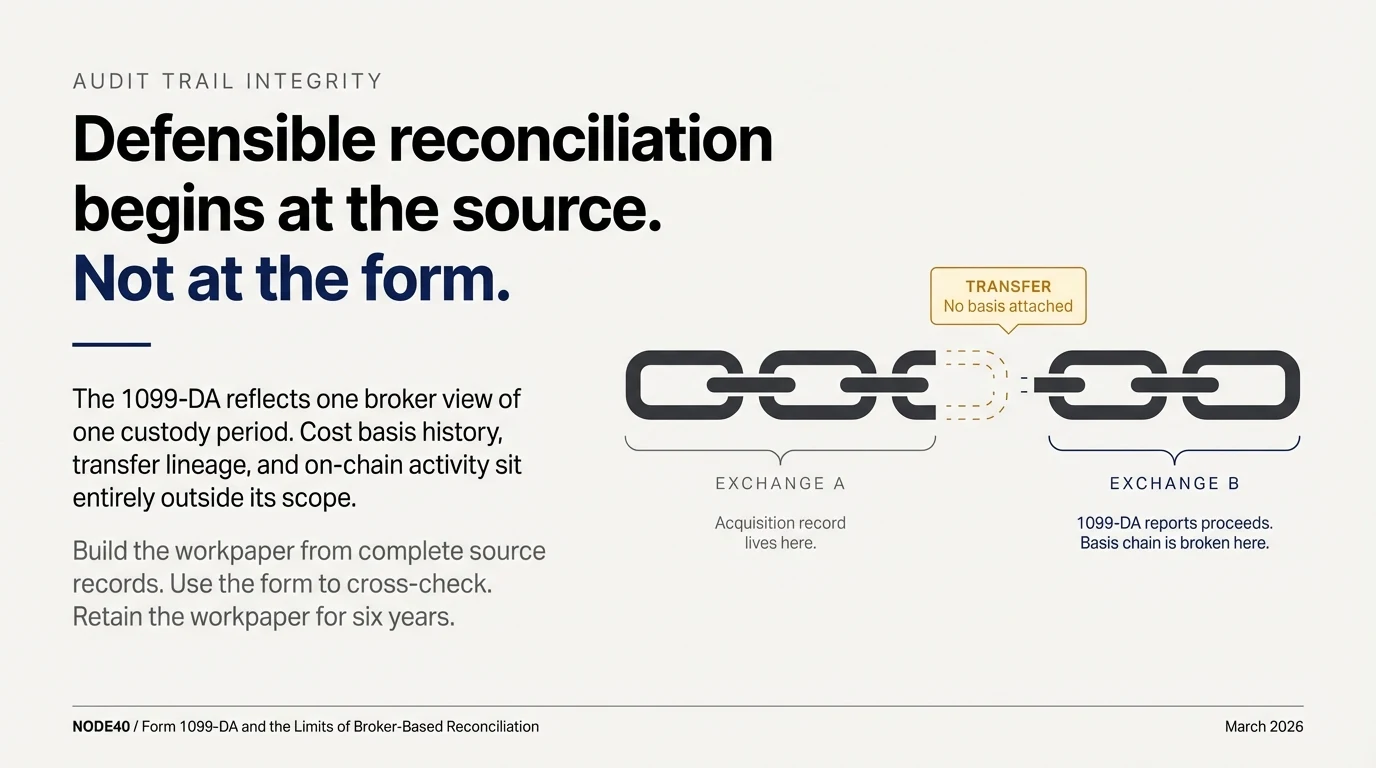

The IRS form title is precise: "Digital Asset Proceeds From Broker Transactions." Proceeds. From one broker. For transactions that broker processed. This is the entire scope of the instrument, and it is a deliberately narrow one. The form tells the IRS what a broker received on a sale, and it tells the taxpayer what the broker recorded. It does not tell anyone what the taxpayer paid to acquire the asset, when they acquired it, which specific lot was disposed, or whether the disposal was taxable in the first place.

The 1099-DA does include a cost basis field, but its utility is limited to assets whose full acquisition history lived within that broker's own custody. The moment an asset entered the broker's platform via transfer from another exchange or from a self-custody wallet, the basis chain is broken. Transferred assets arrive without acquisition history attached, and the receiving broker has no mechanism to know what the taxpayer originally paid. For those assets, the cost basis field will be blank, zero, or flagged as "not reported to IRS" under box 6 of the form instructions, which is the broker's honest acknowledgment of the gap rather than a recoverable data error.

The Multi-Custodian Gap Is Not Solvable by Aggregation

Active digital asset participants routinely maintain positions across multiple exchanges and self-custody wallets. Each custodian generates its own 1099-DA, covering only what it directly processed. No single form, and no combination of forms from different custodians, captures the cross-custodian basis lineage that accurate gain and loss computation requires.

Consider the most common scenario: a taxpayer acquires an asset on one exchange, transfers it to another, and sells it there. The receiving exchange reports proceeds on a 1099-DA with no cost basis because the asset came in as a transfer. The sending exchange reports nothing because there was no disposal on its platform. The taxpayer holds two platforms' export records, but neither 1099-DA contains the full picture, and stacking them does not produce one. The correct basis sits in the original acquisition record at the sending exchange, not in any information return. Aggregating 1099-DAs from multiple custodians does not resolve this problem; it concatenates incomplete records and may obscure the gap by creating the appearance of a complete dataset.

For a detailed look at how this gap plays out operationally for accounting firms serving crypto clients, see The 1099-DA Reconciliation Gap: Why Broker Reporting Captures Only Half of Crypto Activity.

Long-Term Holders Have a Historical Basis Problem the Form Cannot Touch

The 1099-DA reporting regime begins with tax year 2025. Any asset acquired before January 1, 2025 carries basis that was established entirely outside this system. For a long-term holder disposing of Bitcoin or Ethereum in 2025 or 2026, the 1099-DA will carry the proceeds of the sale but no corresponding basis sourced from a 1099-DA-era record. That basis must come from wherever it has always come from: exchange statements, transaction history exports, blockchain records, and prior-year tax workpapers. The form contributes nothing to solving that problem. Given that substantial holdings across the digital asset market were accumulated between 2015 and 2024, the historical basis gap will be present in a large proportion of 2025 returns and will continue to surface for years as those assets cycle through taxable events.

On-Chain and DeFi Activity Is Structurally Outside Broker Reporting

The 2024 final regulations implementing broker reporting requirements (Treasury Decision 10000) apply to centralized exchanges and similar intermediaries. Decentralized protocol transactions, peer-to-peer transfers, staking and liquidity pool activity, airdrop receipts, and self-custody wallet operations are not covered by 1099-DA reporting for tax year 2025. For any taxpayer with meaningful on-chain activity beyond centralized exchange trades, the 1099-DA record will be incomplete not because of a data quality failure but because the scope of the form does not extend to those transaction types. Treating the 1099-DAs received as a complete transaction record when on-chain activity exists creates an invisible gap: the preparer sees what the form covers and may not know what it misses.

The Regulatory Specification Is Still Moving

Two IRS notices published on January 7, 2026 are worth noting for anyone building reconciliation workflows around the current form. The first issued corrections to the 2025 Instructions for Form 1099-DA, specifically addressing de minimis rules for reporting certain sales of digital assets and optional reporting methods. The second announced that Form 1099-DA is excluded from the Combined Federal/State Filing Program for tax year 2025, meaning state-level reporting requires a separate filing and tracking workflow. These are not administrative housekeeping; they reflect a form specification that is still being refined. Reconciliation methodology built tightly around a form that is receiving instruction corrections in January of the filing year carries meaningful implementation risk.

Ingesting 1099-DA Imports the Broker's Errors

When a preparer or compliance team uses the 1099-DA as a primary reconciliation input, they inherit whatever the broker got wrong. Brokers are principally obligated to report proceeds accurately; cost basis is secondary, and the history of 1099-B reporting for conventional securities suggests it takes several years for broker cost basis accuracy to stabilize after a new reporting regime begins. Digital assets present additional complexity: lot accounting is more involved when assets include staking receipts, hard fork allocations, or airdrop events; UTXO-level tracking varies across broker systems; and fee treatment in basis calculations is inconsistently implemented. Errors embedded in a 1099-DA will not announce themselves at ingestion. They will surface later, when the discrepancy appears in a CP2000 underreporter notice.

The Compliance Burden Stays with the Filer

When a taxpayer relies on 1099-DA data that turns out to be incomplete or incorrect, the IRS's CP2000 underreporter process targets the taxpayer. The broker may have issued an erroneous form, but the accuracy obligation belongs to the filer. An incorrect 1099-DA is a potential mitigating factor in a penalty discussion, not a legal defense. For preparers advising institutional or high-net-worth clients, the professional liability follows the accuracy of the reconciliation itself, not the diligence of the data ingestion process. That liability cannot be delegated to the broker.

Part II: What Taxpayers and Preparers Should Do Instead

The appropriate role for Form 1099-DA is as a cross-reference and compliance checkpoint, not as a starting point. Authoritative digital asset reconciliation begins from the blockchain and from complete exchange records, then uses the 1099-DA to verify consistency. Every on-chain transaction is recorded in an immutable, publicly verifiable ledger. The 1099-DA is a filtered, partially abstracted derivative of that ledger, covering one broker's view of one category of activity. Working from the ledger up is more defensible than working from the form down.

Building the Complete Source Set

Before any reconciliation work begins, a preparer or taxpayer needs every relevant record assembled. That means all 1099-DA forms received across all custodians, including any corrected versions. It also means complete transaction history exports from each exchange account in full CSV or API format, not summary tax reports, which often suppress the transaction-level detail needed to verify individual disposals. For self-custody activity, block explorer records or a dedicated on-chain ledger tool are necessary. Prior-year workpapers establishing carried-forward basis for pre-2025 acquisitions are essential for any long-term holder. Transfer records, including withdrawal confirmations from the sending platform and deposit confirmations from the receiving platform, need to be assembled separately because they will not appear on any 1099-DA as a taxable event, yet they frequently appear on the 1099-DA of the receiving broker as though they were.

Working Through Discrepancies Systematically

When the 1099-DA does not match the taxpayer's records, the first task is classification rather than correction. Most discrepancies in tax year 2025 will fall into recognizable categories, and the response to each is different.

- Proceeds that differ from the taxpayer's exchange records for the same transaction point to a data accuracy issue with the broker's reported figure.

- Blank or zero basis where the taxpayer has a documented acquisition record points to a transferred-asset gap.

- A reported disposal that matches the date and amount of a wallet-to-wallet transfer points to a misclassification by the broker.

- Missing transactions entirely, where the taxpayer's own records show disposals not reflected on any 1099-DA, point to on-chain or self-custody activity outside broker reporting scope.

- Duplicate reporting, where the same transaction appears across two platforms, arises from the mechanics of cross-custodian transfers.

- Timing differences near year-end reflect date convention mismatches between broker systems and taxpayer records.

Each category has a different resolution path. Misclassified transfers require documentation of the sending and receiving records to establish that no taxable disposal occurred. Basis gaps require going back to the original acquisition record. Timing differences are typically resolved by obtaining the blockchain transaction hash, which carries an on-chain timestamp, and applying it consistently.

The Transfer Check Should Come First

In practice, the most productive first step in reconciling a 1099-DA against a taxpayer's records is to check every discrepancy against the transfer history before assuming a data error. Transfers between accounts or wallets appear to the receiving broker as inbound positions, and if the broker cannot confirm those positions were acquired at the platform (they were not), it may report them with zero or blank basis. When the taxpayer then reports a gain calculated from the actual acquisition basis, the proceeds figure matches the 1099-DA but the basis does not, which looks like a discrepancy but is actually correct. The resolution is documentation: the withdrawal record from the sending platform, the deposit confirmation at the receiving platform, and the on-chain transaction record linking them. That documentation package, retained in the workpaper file, supports the correct basis treatment and explains why the 1099-DA basis field was not used.

Basis Method Consistency Requires Active Verification

Brokers apply a default lot identification method, most commonly FIFO, unless the taxpayer has communicated a different election in writing before the disposal. If a taxpayer has been using specific identification or HIFO and that election was not confirmed with the broker in advance, the broker's basis figure will reflect a different lot than the taxpayer's records, producing a discrepancy even when the underlying transaction data is accurate. The preparer's task is to confirm that the taxpayer's elected method was validly communicated, that it qualifies under current IRS guidance, and that it was applied consistently across the same asset class for the tax year. Where method differences explain a basis mismatch, the workpaper should document the election, the resulting calculation, and the basis for treating the taxpayer's method as controlling.

Timing Boundaries Deserve Specific Attention

A transaction executed near midnight on December 31 may carry different dates depending on whether the broker records trade date, settlement date, or blockchain confirmation timestamp, and may fall in different tax years depending on that convention. The blockchain timestamp is the most defensible reference point for digital assets because it is independently verifiable and immutable. For any near-boundary transaction where the 1099-DA and the taxpayer's records reflect different tax years, the resolution should start with pulling the transaction hash from a block explorer, confirming the UTC timestamp, and applying the date consistently across all records. This category of discrepancy is among the most common triggers for CP2000 notices and among the most straightforward to resolve if the blockchain record is retrieved contemporaneously.

Documenting a Reasonable-Cause Position When Resolution Is Not Possible

Some discrepancies will not be fully resolvable before the filing deadline. Historical records may be incomplete. A broker may have issued an erroneous form that has not been corrected yet. The tax treatment of a specific transaction type may be subject to open IRS guidance. In these cases, the filing position should be supported by a reasonable-cause analysis in writing. That analysis should describe the nature of the discrepancy and why it could not be resolved, document the steps taken to obtain correct information (contact logs, data requests, blockchain lookups), state the taxpayer's best-available estimate of the correct figure and the methodology behind it, and note the status of any pending corrected forms. This does not guarantee penalty protection, but it is the standard component of a defensible position when the information environment is incomplete. If a corrected 1099-DA arrives after filing, the preparer should evaluate whether the change is material enough to warrant an amended return.

Retention Standards

The IRS statute of limitations for assessment is generally three years from the filing date, extended to six years when gross income is omitted by more than 25 percent. For returns with material digital asset activity, a six-year retention floor is appropriate. The preparer's file should include:

- Every 1099-DA received, including corrected versions

- The reconciliation workpaper mapping each 1099-DA line to the corresponding Form 8949 entry, with a category and resolution status for each discrepancy

- Source records used to resolve each discrepancy

- Notes on any unresolved discrepancy and the reasonable-cause analysis supporting the filing position

- Documentation of any taxpayer elections relevant to the return

The workpaper should be structured so that a reviewer who was not involved in the preparation can reconstruct the logic of every adjustment made to the 1099-DA data.

How to Reduce CP2000 Risk in Practice

There is no method that eliminates the possibility of receiving a CP2000 underreporter notice. The IRS generates them algorithmically by comparing amounts reported on information returns, including 1099-DA, against amounts reported on the tax return, and any unexplained discrepancy can produce one. What a preparer can control is the quality and completeness of the position taken on filing, and a disciplined pre-filing process reduces both the probability of receiving a notice and the effort required to respond if one arrives.

The first and most direct risk factor is incomplete proceeds reporting. The IRS will have the 1099-DA data before it reviews the return. If the return omits or understates proceeds that appear on a 1099-DA, a notice is likely. The practical response is to ensure that every disposal captured on any 1099-DA received by the taxpayer is accounted for somewhere in the return, either reported as a taxable disposal on Form 8949 or documented as a non-taxable event (such as a confirmed internal transfer) with supporting records retained in the file. The goal is not to match the 1099-DA figures uncritically; it is to ensure that nothing on the 1099-DA is simply absent from the return without explanation.

The second risk factor is unresolved basis discrepancies that produce a gain figure the IRS cannot reconcile to the broker's reported data. A line-level mapping from each 1099-DA entry to the corresponding Form 8949 line, with a documented status for every discrepancy, gives the preparer confidence that the return is internally consistent and gives the taxpayer a defensible starting point if the IRS asks questions. Discrepancies that are explained and documented in the workpaper, even if they result in a different basis or gain figure than the 1099-DA implied, are far easier to respond to than discrepancies that were not noticed before filing.

The third factor is what happens when a discrepancy cannot be resolved before the filing deadline. A written reasonable-cause memo, even for a single unresolved item, demonstrates that the preparer identified the issue, took specific steps to resolve it, reached a best-available estimate using a documented methodology, and did not simply ignore the discrepancy. If a CP2000 notice follows, that memo is the starting point for the response. It also supports a request for penalty abatement if the IRS determines the reported amount was incorrect, because it shows the error was not the result of negligence or intentional disregard.

Part III: The PII Risk of Uploading and Storing 1099-DA Files

Form 1099-DA is not a benign summary. It carries the taxpayer's legal name, mailing address, and taxpayer identification number, which for individual filers is the Social Security Number. It also contains the broker's account number for the taxpayer, the asset description, transaction-level proceeds, and, where reported, cost basis. Together these fields constitute a structured record that links a real, identified person to specific financial transactions. The exposure of this document to unauthorized parties carries the same risk as the exposure of any other sensitive tax record, and in some respects more risk, because it also encodes financial behavior in addition to identity.

The risk is not hypothetical. When taxpayers upload 1099-DA files to consumer-oriented portfolio tracking or tax preparation platforms, they are transmitting those records to services whose privacy policies permit data uses that many institutional compliance contexts would not accept. A review of privacy disclosures from major consumer crypto tax platforms reveals several consistent patterns.

These platforms routinely collect not just the uploaded tax data but also wallet addresses, exchange-linked transaction history, and device and behavioral data about how the user interacts with the service. They share this data with third-party analytics providers, including session recording tools that observe user behavior on the platform, and with advertising technology partners for purposes including interest-based advertising and the creation of "lookalike audience" profiles on external platforms. Financial behavior within the product, including what assets a user holds and their tax position, is treated as a signal for external ad targeting under these arrangements. Data is also described as transferable in the event of a business sale, acquisition, financing, bankruptcy, or dissolution, with no user opt-out provided for those scenarios. Retention periods are frequently unspecified, and security disclosures typically include explicit disclaimers that no system is fully secure and that the platform accepts no liability for unauthorized access to personal data outside its reasonable control.

None of this is necessarily unlawful. Consumer platforms are not bound to institutional data standards. But taxpayers and preparers handling 1099-DA files on behalf of clients should evaluate these terms before routing sensitive tax records through services operating under them. The practical controls are straightforward: understand what the platform's privacy policy permits before connecting accounts or uploading documents; prefer platforms with defined data retention limits and without advertising or analytics data-sharing relationships; ingest only the fields required to support reconciliation rather than storing full-form copies in environments with broad third-party access; and treat the 1099-DA file with the same handling discipline applied to any document carrying a Social Security Number. For preparers operating under professional obligations, data minimization is not just prudent practice; it is a component of the duty of care owed to the client.

Conclusion

Form 1099-DA represents a meaningful development in digital asset tax administration. It will, over time, improve voluntary compliance and give the IRS better visibility into a historically opaque asset class. But the form's utility to the IRS as a reporting instrument is not the same as its utility to a taxpayer or preparer as a reconciliation tool. The structural limitations are real and will not be resolved by better ingestion technology or more platforms supporting the format: a single-custodian information return reporting proceeds cannot reconstruct cross-custodian basis history, pre-2025 acquisition records, or activity that is outside broker reporting scope.

The correct approach is to treat the blockchain and complete exchange records as the primary source, build the reconciliation from those, and use the 1099-DA to cross-check and flag discrepancies. When discrepancies appear, resolve them methodically, document the resolution, and retain the workpapers for at least six years. When they cannot be fully resolved, document a reasonable-cause position. That process produces a return that is defensible. Relying on the 1099-DA to replace it does not.

For more on the operational side of this challenge, see The 1099-DA Reconciliation Gap. For information on NODE40's source-first reconciliation infrastructure, visit our crypto tax and 1099-DA platform page.

Informational only. Not legal, tax, or accounting advice. Consult a qualified professional for guidance specific to your situation.

Sources

- IRS, About Form 1099-DA, Digital Asset Proceeds From Broker Transactions. Page last reviewed January 20, 2026; accessed March 9, 2026.

- IRS, Instructions for Form 1099-DA (2025). Corrections issued January 7, 2026 (de minimis rules; optional reporting methods).

- IRS notice: Form 1099-DA excluded from Combined Federal/State Filing Program for tax year 2025. Published January 7, 2026.

- IRS, Internal Revenue Code Section 6501 (statute of limitations for assessment).